Pan Pan Pan: Building Your Emergency Fund Lifeboat

Start 2025 right. Don’t wait for a financial Mayday— create your safety net today!

Dear Yachtie Investors,

Ahoy, my fellow yachties! I recently had a big scare onboard that could’ve ended up a lot worse. This got me thinking- am I prepared to cover myself financially if the proverbial shit hits the fan?

After setting clear financial goals (Step 1 of our Financial SOPs), it’s time to build your safety net: the Emergency Fund. Life at sea can be as unpredictable as the ocean—contracts end suddenly, injuries happen, and sometimes you just need to step back to recharge. That’s where an emergency fund becomes your lifeboat.

Before we dive in: check out our full website & service catalogue here.

Why You Need an Emergency Fund

Yachting is a unique and volatile industry. Contracts can end abruptly, or an unexpected situation might force you off the boat. Having a rainy-day fund ensures you’re not scrambling to make ends meet when life throws you a curveball.

For us yacht crew, this fund isn’t just about replacing your income—it’s about maintaining stability in the “real world” when you’re back on land.

For those with families, the stakes are even higher. Mortgage payments, school fees, and other fixed costs don’t pause when life gets rocky. You may need to aim for the upper range of 6 months or even beyond to cover these responsibilities.

How Much Should You Save?

The golden rule: 3 to 6 months of land-based expenses. While we often don’t have living expenses onboard (thanks, free room and board!), life on land is a whole different game. Let’s break it down:

Why Land-Based Expenses?

Once off the boat, you’ll need to cover essentials like rent, utilities, groceries, transportation, and health insurance.

How to Calculate Your Target Fund:

Total up what you’d spend monthly if you lived on land in your home country or a country where you might relocate.

Multiply that by 3 to 6 months. Boom, that’s your safety net goal.

Avoid the Inflation Trap:

While it’s important to keep your fund in a liquid, low-risk account, don’t let it grow excessively beyond its purpose. Excess cash loses value to inflation and represents an opportunity cost—funds you could otherwise invest for growth.

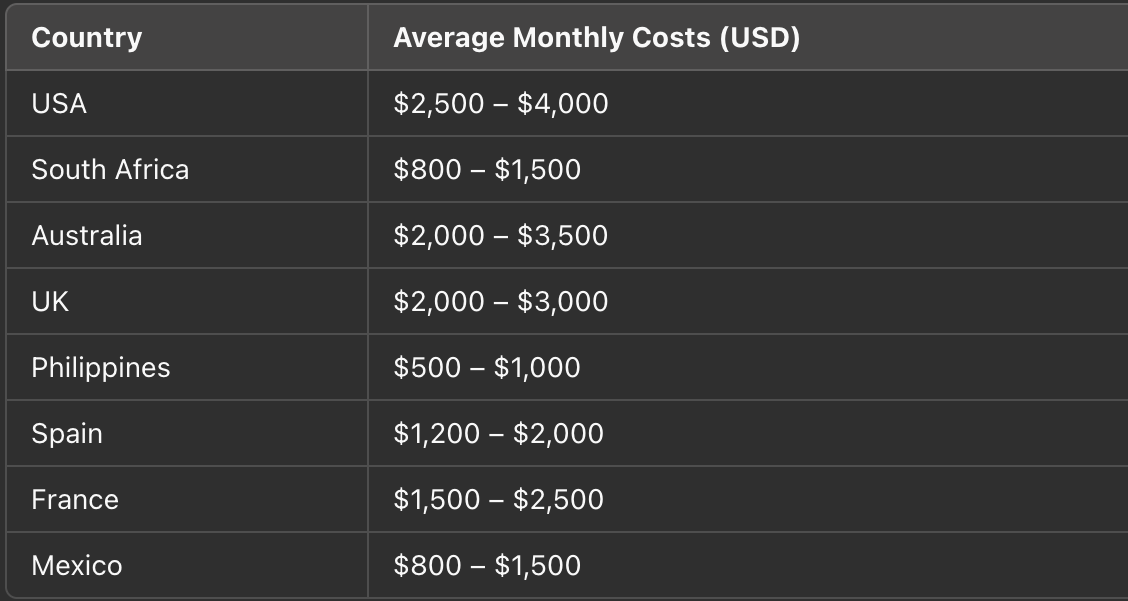

Living Expenses Comparison by Country

(Keep in mind these are general averages for the most common yacht crew demographics—your actual costs might vary based on lifestyle and location.)

Pro Tips for Building Your Fund

Start Small and Automate:

Set aside a portion of each pay check into a high-yield savings account. (South Africans can reach out to me to set up a savings account with Discovery Bank). Even $100 per month builds up over time.

Use Bonuses Wisely:

Instead of splurging on a new gadget, put at least 50% of your annual bonus into your emergency fund.

Keep It Accessible but Separate:

Your emergency fund should be easy to access in a pinch, but not mixed with your regular checking account to avoid temptation.

Stay Disciplined:

This fund is for true emergencies, not for upgrading your dive gear or financing a weekend in Ibiza!

Peace of Mind in a Volatile World

Having an emergency fund isn’t just about the money—it’s about confidence. It’s knowing you can weather any storm without panicking. For yachties like us, who live a life of adventure and unpredictability, this safety net is non-negotiable.

So, start today. Your future self—the one chilling on a beach in Spain or taking a breather back home in South Africa—will thank you.

What’s Your Big Goal for 2025?

As we sail into the new year, I’d love to hear from you. What’s your top financial goal or biggest dream for twenty 2025? Hit reply and let me know—I’ll share some in the next newsletter to keep us all motivated.

Here’s to another year of growth, opportunity, and making waves!

Fair winds and following seas,

Charl (aka Gnarly Charly, your finance first mate)

P.S. If you missed any of the top reads from this year, I’ve compiled them here:

Let’s kick off 2025 with focus and fire!

Buoy’s , Balance & Banter

Your weekly dose of ideas to keep you steady, inspired, and smiling—whether you're charting your financial future or just riding the waves.

Good Read of the Week

📖 Article: How to Become a Millionaire in Your 20’s.

Dan Koe’s article emphasizes the importance of focusing on high-value skills and leveraging the internet to build scalable income streams in your 20s. By cultivating discipline, optimizing your time, and reinvesting profits into yourself or your business, you can set the foundation for financial independence and long-term wealth.

Words to Live By

💡 Quote: "The secret of getting ahead is getting started." - Mark Twain

A perfect fit for yachties taking the first steps toward financial security!

Just for Laughs

😂 Video: Llama Drama

Trust the Aussie’s to deliver a goldie like this.

I would suggest to keep your emergency fund in a High Yield Savings Account and never with a traditional bank, ex. Chase, BofA, etc. Keeping your money with these banks is a sure way to lose to inflation. HYSA can offer 4% APY and upward. Traditional banks barely offer 1% APY. This is coming from an American, so I am not sure if this works in other countries.